Search and contract data show a clear split between business and personal leasing demand in 2025.

Consumer finance volumes remain significantly higher than business volumes, yet the direction of travel is diverging.

This piece draws on market data and industry reports released by Google and Statista.

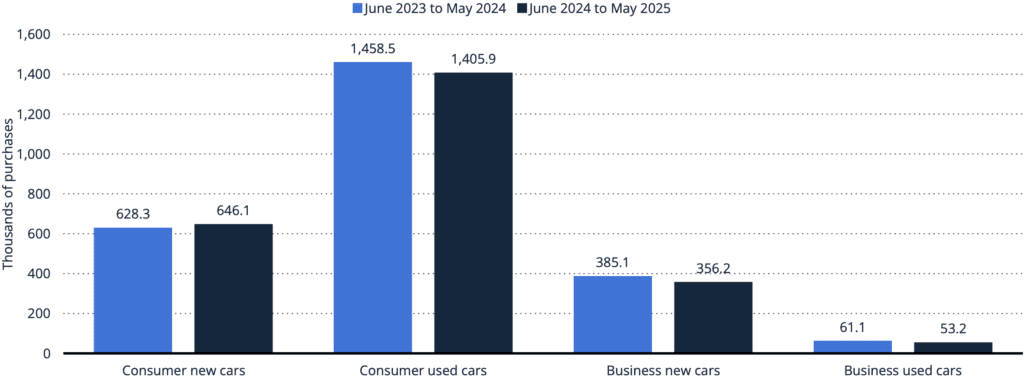

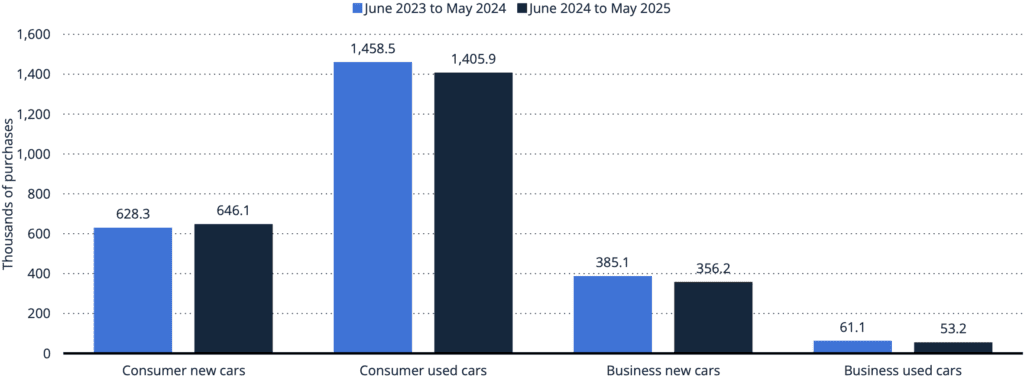

Cars bought on finance by consumers and businesses in the UK 2023-2025:

This chart shows consumer finance volumes softening slightly year-on-year, while business volumes decline more modestly.

This reflects how different the two audiences are reacting to the same economic conditions.

For automotive businesses, this changes where demand can be captured and where budget is at risk.

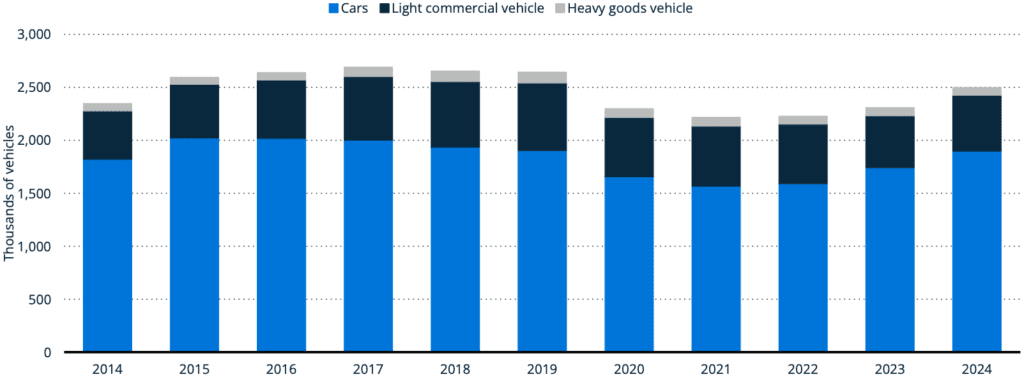

Business Leasing Demand Is Proving Structurally Strong

Fleet data shows that corporate leasing volumes are holding at scale despite market pressure.

Total fleet size of BVRLA members in the UK 2014-2024, by type:

The corporate fleet sits at around 2.5 million vehicles in 2024, with only marginal movement year-on-year.

This stability comes from how businesses make vehicle decisions. Vehicles sit inside operating budgets and are tied to revenue generation, service delivery, or employee benefits.

That keeps demand active even when costs rise.

For leasing brokers and funders, this means business demand remains predictable and easier to convert.

Budget should reflect this stability.

More investment should move into channels and campaigns that target business users, including fleet decision-makers, SME owners, and salary sacrifice audiences.

Measurement should prioritise contract value and pipeline quality over raw lead volume.

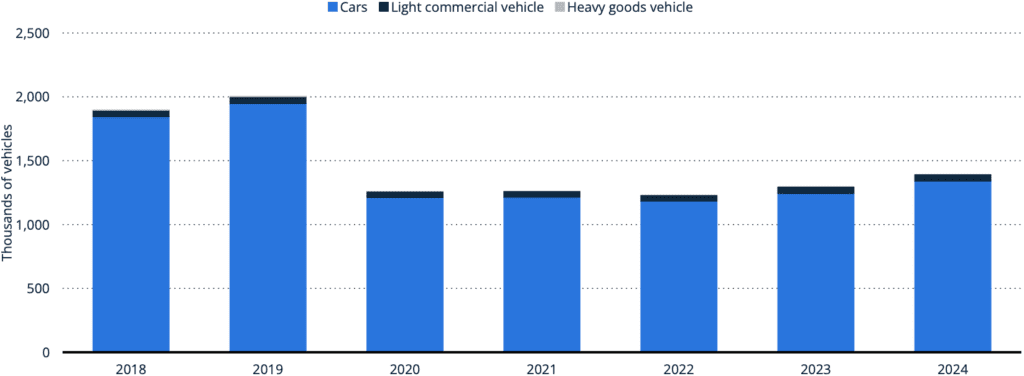

Personal Leasing Is Recovering More Slowly Than Expected

Personal leasing volumes are still below pre-2019 levels despite recent growth.

Personal contracts fleet size of BVRLA members in the UK 2018-2024, by type:

The personal contract fleet sits at 1.39 million vehicles in 2024 and remains below its 2019 peak.

This shows that recovery in consumer leasing has not kept pace with the wider market.

Higher interest rates are pushing monthly payments up, which directly affects affordability.

This reduces both willingness and ability to commit to fixed monthly costs.

For automotive brands focused on personal leasing, this creates a clear efficiency problem.

Budget spent on broad consumer demand is producing weaker returns.

Activity should shift toward high-intent search, in-market audiences, and offer-led messaging with clear monthly pricing.

The Gap Is Widening Because Decision Drivers Are Different

Business and personal leasing are diverging because they are driven by different decision frameworks.

The financing split reinforces this difference.

Cars bought on finance by consumers and businesses in the UK 2023-2025:

The data shows over 1.4 million used vehicles financed by consumers compared to just over 50,000 by businesses.

Consumer demand is heavily weighted toward used vehicles and price sensitivity.

Business demand is more evenly spread across new vehicles and structured contracts.

In a high-cost environment, this creates separation in how demand behaves.

For automotive businesses, this requires a split strategy.

Channel mix, messaging, and targeting should be separated clearly between business demand capture and personal demand generation.

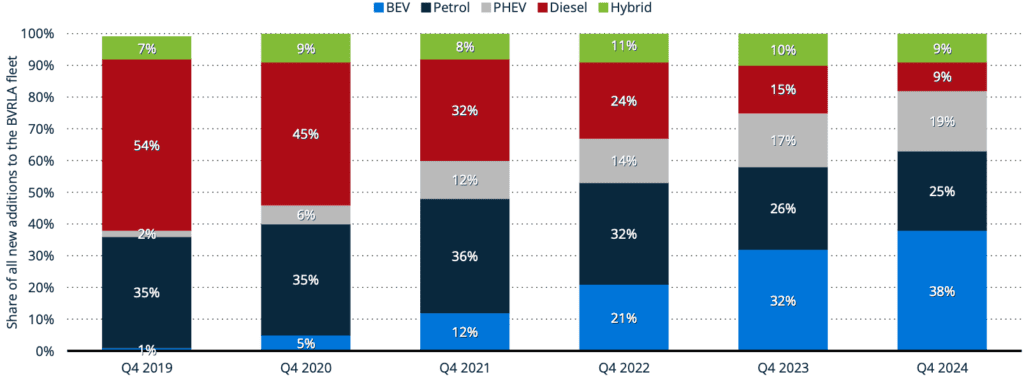

EV Adoption Is Being Carried by Business Leasing

Fleet data shows that EV adoption is accelerating quickly within leasing fleets.

Distribution of new cars added to the BVRLA fleet in the UK 2019-2024, by fuel type:

Battery electric vehicles have grown from a negligible share in 2019 to a material proportion of new fleet additions by 2024.

This shift is being driven through leasing structures.

Businesses are using leasing to manage upfront cost while benefiting from tax efficiency and lower running costs.

This concentrates EV demand within business leasing channels.

For OEMs and leasing providers, this has a direct implication.

EV marketing should lean into business audiences, including company car drivers, fleet managers, and SME operators.

Personal EV demand remains more price-sensitive and slower to convert.

Budget allocation should reflect where EV adoption is actually happening.

What Automotive Businesses Should Do Next

The data shows that leasing demand is shifting toward business users while consumer demand remains under pressure.

Industry turnover continues to grow, with a £1.7 billion increase in 2023, showing that value is still being created despite demand pressure.

This growth is being supported by structurally stronger segments, including business leasing.

Automotive businesses should increase budget exposure to business leasing demand, tighten targeting on personal leasing to protect efficiency, align EV strategy with business-led adoption, and separate measurement between business and personal performance.

If this pattern is visible in your own data, the priority is to realign spend with where contracts are still being written.

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information