The UK car leasing market today is often described in simple terms. There is a slowing demand, rising costs and the transition to electric. But when you dig into the actual data, a more nuanced picture appears.

What we are seeing instead is a market reshaped by affordability pressure, the rise of used vehicles and more informed, comparison-driven buyers.

This piece draws on market data and industry reports released by Google and Statista.

A Market Still Growing but Not Evenly

At a headline level, the UK automotive and leasing industry remains large and active.

- Passenger car sales reached 1.81 million vehicles in 2024

- Total passenger car revenue sits at $54.8 billion in 2025

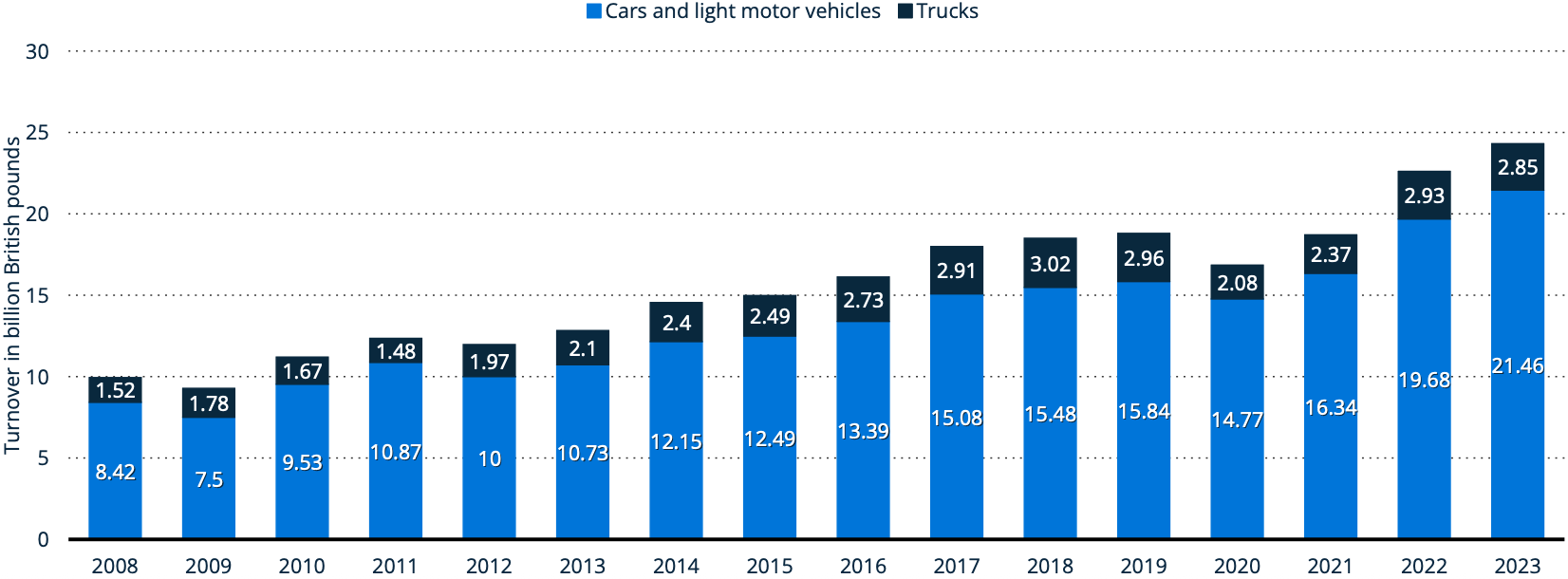

- The vehicle rental and leasing sector has seen steady long-term turnover growth, reaching over £21 billion for cars and light vehicles in 2023.

Vehicle renting and leasing turnover in the UK 2008-2023 by segment:

This is important because leasing is structurally tied to overall vehicle sales and finance availability.

But the growth isn’t even, as the market is splitting across:

- New vs. used

- Consumer vs. business demand

- Premium vs. value-led segments

Leasing vs. Car Finance

The biggest misconception is that leasing is separate from car finance.

In reality, leasing is just one part of a much larger vehicle financing industry. Furthermore, the data shows that finance is dominating user behaviour.

According to the Finance and Leasing Association data (page 6):

- Over 2 million cars were bought using finance in the year to May 2025

- Around 1.4 million financed vehicles were used cars for private or personal buyers

- Around 646,000 financed vehicles were new cars for private customers

Cars bought on finance by consumers and businesses in the UK 2023-2025:

What this tells us:

- Financing, not outright purchase, is still the default choice

- Leasing competes directly with loans, PCP and HP products

- Used cars account for the majority of financed vehicle purchases

Leasing brands are not just competing with each other – they are competing with the entire finance market.

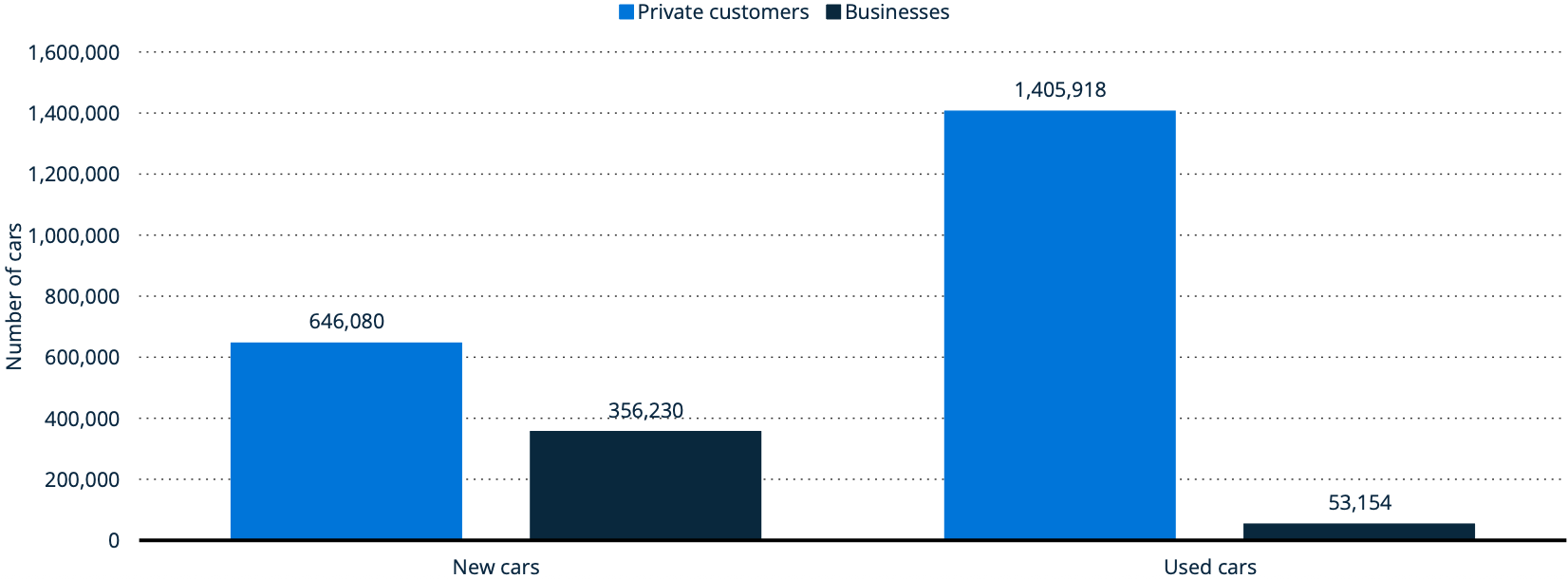

The Used vs. New Divide Is Reshaping Leasing

One of the most important shifts recently is the dominance of used cars. From the same dataset on page seven, we can see that:

- Used cars account for more than twice the volume of new cars in financed purchases

- Private buyers overwhelmingly choose used vehicles over new

Cars financed in the UK by consumer and vehicle type 2024-2025:

This creates a challenge for the leasing industry – leasing traditionally relies on new vehicle supply, but demand is shifting toward lower-cost options.

This means leasing growth isn’t constrained by car demand, but by what consumers can afford to lease new vs. finance used.

Affordability Pressures Push Drivers to Delay Purchases and Compare More Aggressively

To understand recent consumer behaviour, we looked at pricing and credit data:

- Typical car loan APRs sit around 5.8% to 6.4% in 2025.

- Smaller loan amounts can exceed 10% to 13% APR.

Representative APR of 10k GBP car loans by selected banks in the UK 2024-2025:

At the same time:

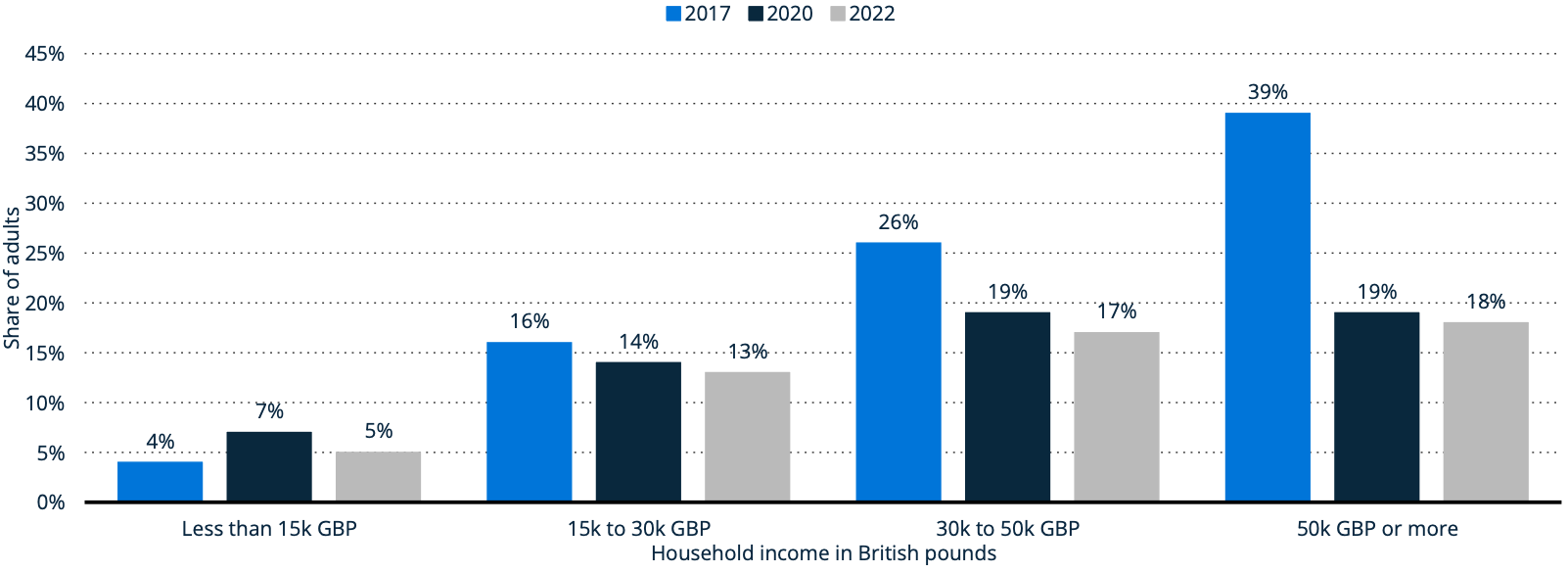

- High-income households still use car finance products more than any other group

- The lower the income, the less likely consumers are to use car finance, suggesting there is a financial barrier here.

Car finance ownership in the UK from 2017-2022, by household income:

This divides the market into:

- Affluent buyers still financing new vehicles

- Value-conscious buyers shifting to used vehicles, comparing products aggressively or delaying purchases entirely

With Rising Costs, Today’s Consumer Behaviour Is Much More Comparison-Driven

Modern car buyers are highly research-driven. The GWI data says:

- 55% use search engines for research

- 39% discover brands via search

- 64% visit brand websites before purchase

And critically:

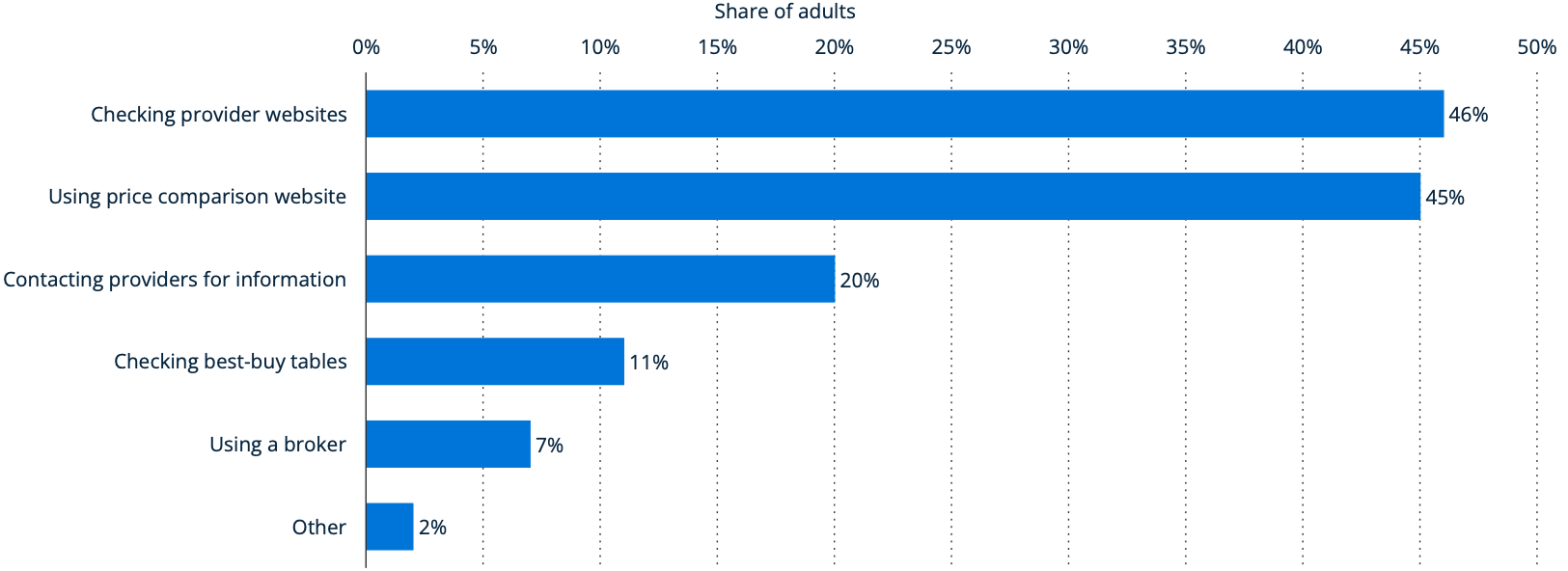

- 45% of consumers use comparison websites when choosing financial products.

Methods to compare motor finance providers in the UK 2022:

This means:

- Leasing is no longer mainly shaped by the dealership. Buyers now research, compare, and evaluate options online before speaking to a salesperson.

- It is a digitally evaluated financial product, people are judging leasing the same way they’d judge a loan, insurance policy, or mortgage product online.

Buyers are comparing:

- Monthly cost

- Total cost of ownership

- Flexibility vs. ownership

- Brand trust and reputation

Business Leasing: Scaled at the Top and Fragmented Below

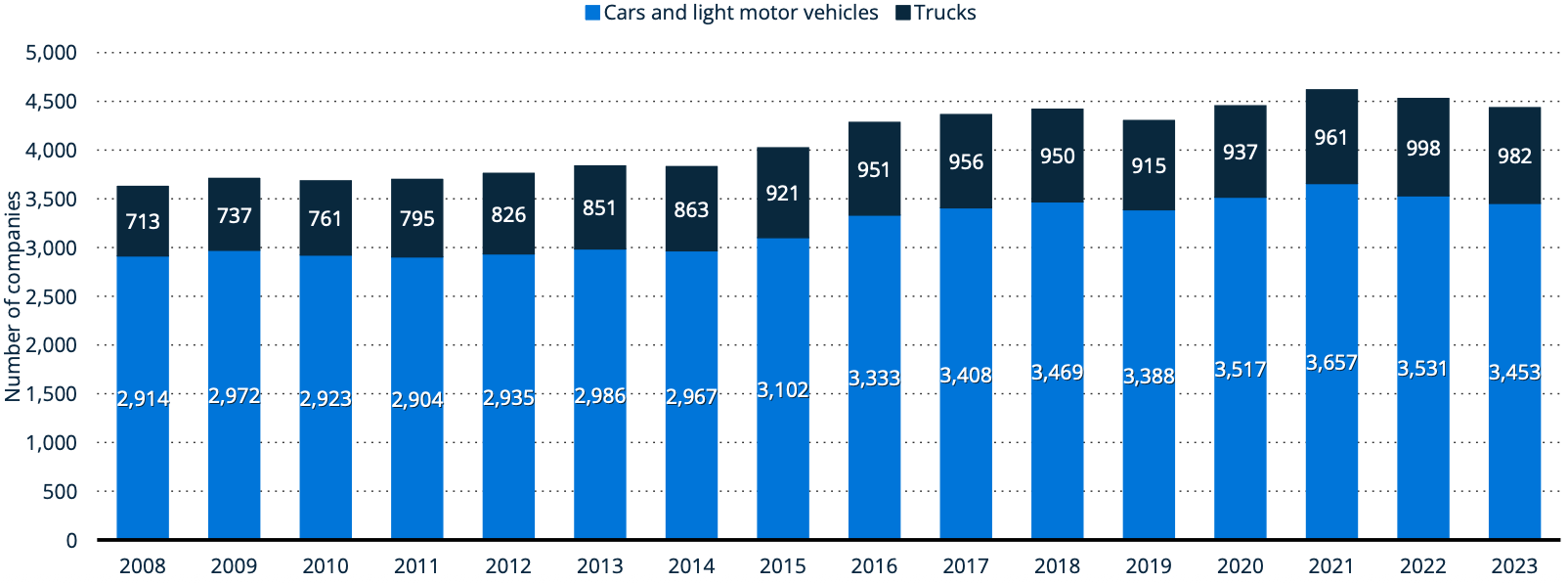

The leasing industry is large but fragmented.

- Over 3,400 leasing companies operate in the UK

- Most are small businesses with 0 to 4 employees

- Yet major players control massive fleets of over 200,000 vehicles each

Number of vehicle renting and leasing companies in the UK 2008-2023:

Meanwhile:

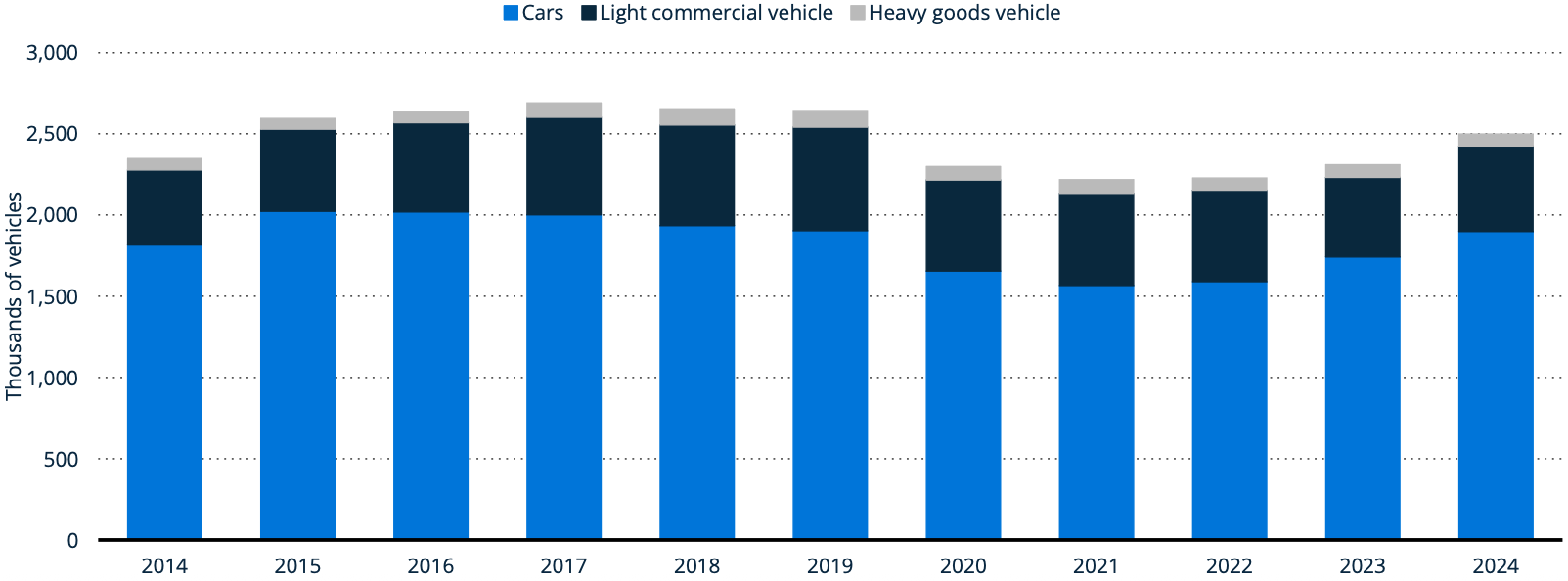

- Total BVRLA fleet exceeds 4 million vehicles

- Corporate leasing alone accounts for around 2.5 million vehicles

Corporate lease fleet size of BVRLA members in the UK 2014-2024:

This creates a market where a few major players dominate at the top, while thousands of smaller leasing firms compete in the middle. The result is constant pressure on price, because buyers can compare similar offers more easily than ever.

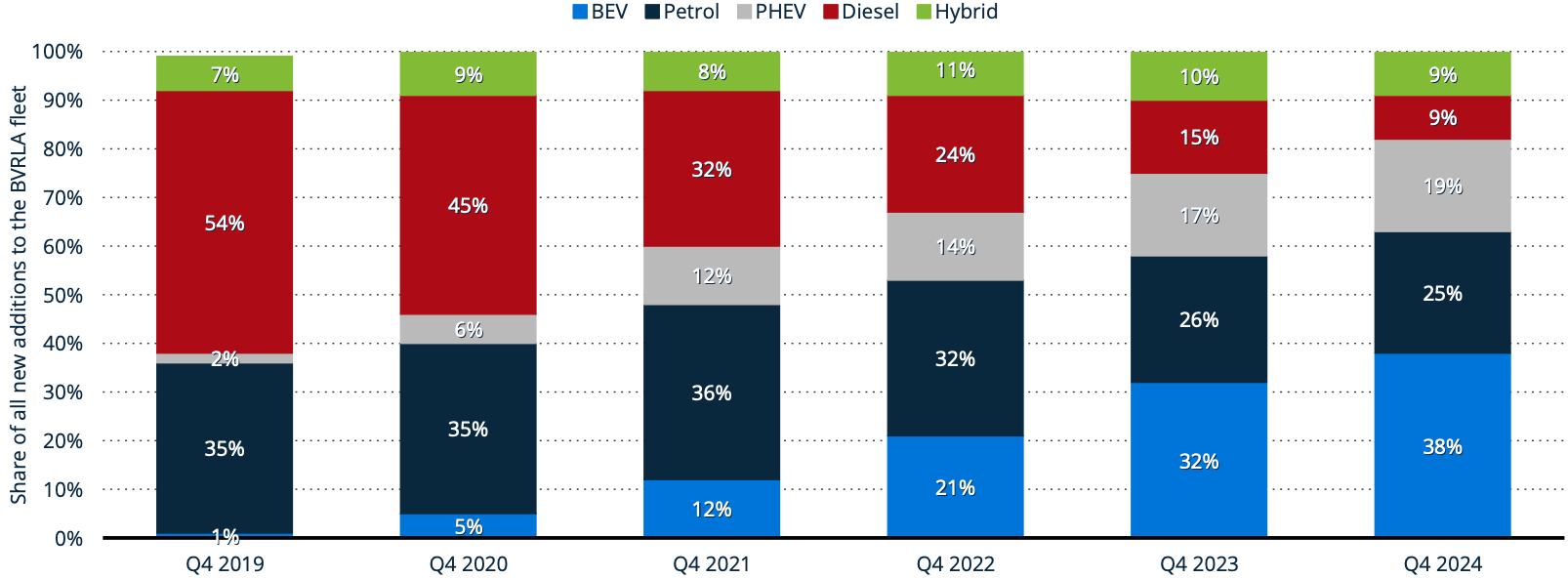

The EV Transition Is Accelerating Leasing’s Role

Leasing is becoming even more important because of electrification. In 2024, battery electric vehicles rose from 1% of fleet additions in 2019 to 38%.

Distribution of new cars added to the BVRLA fleet in the UK 2019-2024, by fuel type:

What’s more, forecasts suggest:

- Around 30% growth in BEV fleet by 2025

- Declining petrol and diesel share

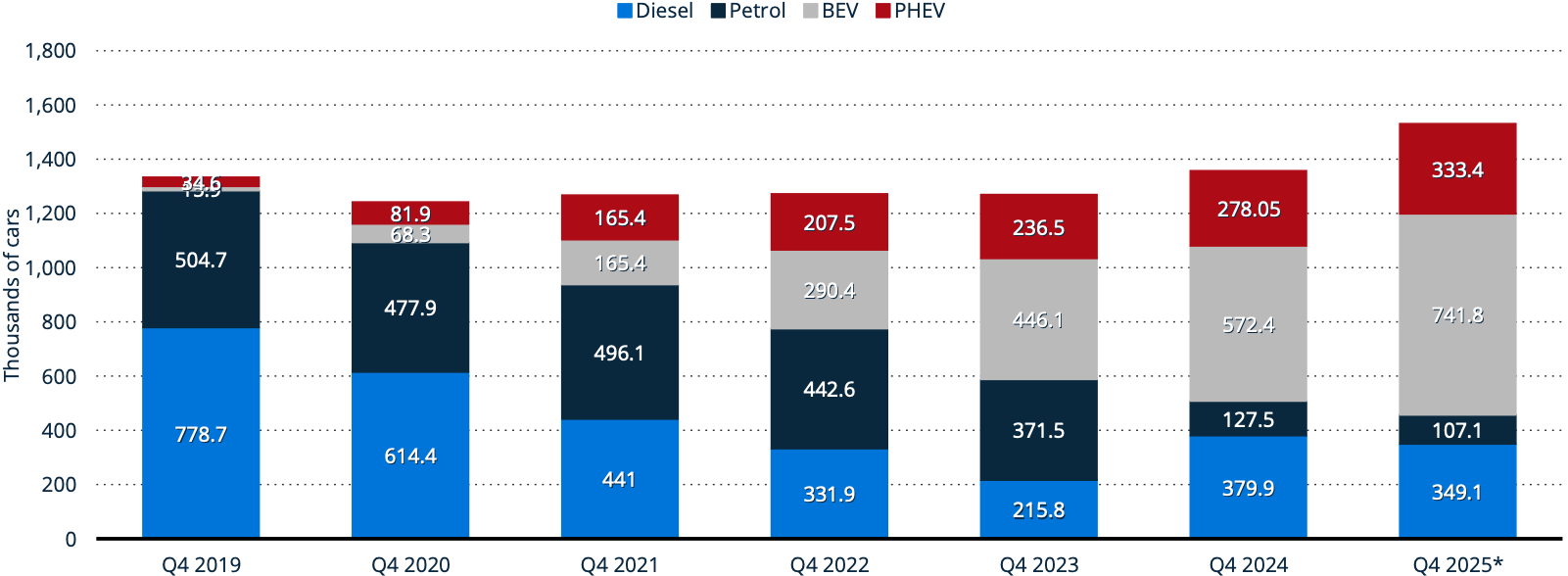

Size of BVRLA fleet in the UK 2024-2025, by fuel type:

While electric vehicles are expensive up front, leasing reduces risk around battery costs, depreciation and changes in technology. As a result, leasing is much more aligned with the mass switch to electric.

So What Is Actually Happening in 2026?

1. Growth hasn’t disappeared, but it’s shifted

The market is still large and active, but the growth is concentrated in:

- Used vehicles

- Finance-driven purchases

- Electric vehicle-related leasing

2. Leasing is competing harder than ever

There’s not just competition with other leasing firms, but against:

- Used car purchases

- Traditional finance products

- Delayed ownership

3. Affordability pressure has a huge impact on consumer behaviour

Higher APRs and cost-of-living constraints mean:

- Buyers are more cautious

- Monthly payments matter more than ever

- Value perception drives decisions

4. Customers are much more likely to visit a brand’s own website than use a broker

Brand and comparison sites dominate the buyer journey when choosing a car, as these are critical for comparing trust, reputation and monthly costs.

What This Means for Leasing Brands

Today, there is still an opportunity for leasing brands, but only if they can:

- Compete on clear value, not just price

- Emphasise monthly affordability and transparency

- Support comparison-friendly journeys

- Lean into electric vehicle leasing as a growth driver

- Build long-lasting trust with their audience

Final Thoughts

The UK car leasing market is maturing, not shrinking. Opportunities still exist, but they’re no longer driven by easy credit or default upgrades to new cars. Instead, it’s driven by a more deliberate buyer, who is:

- More informed

- More cautious

- More focused on value than ever before

The leasing companies that are ready for these customers will be the ones who succeed.

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information