The gap between business and personal leasing is widening across fleet size, finance demand and EV adoption.

- Business finance has created a more stable base for OEMs

- Personal leasing providers should focus on clear value and cost to drive conversions

- Separating personal and business leasing reports will reveal where growth sits

- Leasing companies should focus on EV lease deals for businesses

Business leasing is holding volume while personal demand softens

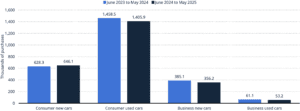

Business vehicle financing volumes are holding more consistently than consumer demand.

The data shows that 409,400 vehicles were financed by businesses in the year to May 2025, while consumer finance remains heavily weighted toward used vehicles.

Cars bought on finance by consumers and businesses in the UK 2023-2025:

This matters because business leasing gives brokers, funders and OEMs a more stable demand base.

Marketing budget should reflect that, with more spend directed toward fleet, SME and company car demand capture.

Personal leasing is under pressure from affordability

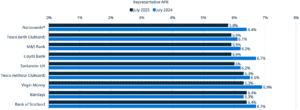

Personal leasing is more exposed to monthly payment pressure.

Representative APRs for car loans remain around 5.8% to 6.4% across major lenders in 2025, which keeps affordability tight for private customers.

Representative APR of 10k GBP car loans by selected banks in the UK 2024-2025:

Motor finance ownership has also fallen among higher-income households since 2017, which reduces the pool of consumers most likely to finance new cars.

Leasing providers should treat personal leasing as a more selective market and focus messaging on total monthly cost, deposit flexibility and clear value.

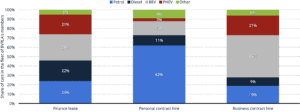

Corporate leasing is carrying fleet scale

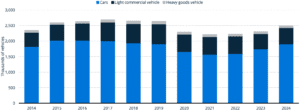

Corporate leasing remains the larger and more reliable fleet base.

The BVRLA corporate leasing fleet reached around 2.5 million vehicles in 2024.

Corporate lease fleet size of BVRLA members in the UK 2014-2024:

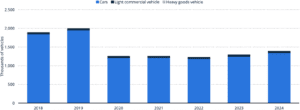

Personal contract fleets reached 1.39 million vehicles in 2024 and remain below 2019 levels.

Personal contracts fleet size of BVRLA members in the UK 2018-2024, by type:

This shows where scale is sitting in the market.

Leasing companies should separate business and personal performance reporting, because blended reporting will hide where growth is actually coming from.

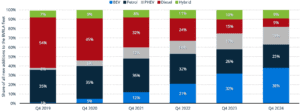

EV adoption is moving faster through business leasing

Business leasing is now one of the clearest routes for EV growth.

Battery electric vehicles accounted for 45% of cars in business contract hire fleets in 2024, compared with a much lower share in personal contract hire.

Distribution of the car fleet of BVRLA’s members in the UK 2024, by fuel type:

Across new BVRLA fleet additions, BEVs increased from 1% in Q4 2019 to 38% in Q4 2024.

Distribution of new cars added to the BVRLA fleet in the UK 2019-2024, by fuel type:

This means EV demand is being pulled forward by fleet policy, benefit-in-kind incentives and business replacement cycles.

OEMs and leasing brokers should prioritise EV content, pricing pages and paid search around business leasing use cases.

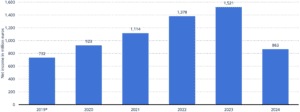

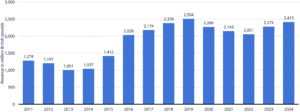

Leasing income is concentrated around large fleet-led providers

The commercial value of leasing is increasingly visible in fleet-led businesses.

Volkswagen Financial Services more than doubled UK leasing income between 2019 and 2023, reaching over €1.5 billion.

Volkswagen’s net income from leasing transactions in the UK 2019-2023:

Lex Autolease revenue reached £2.4 billion in 2024.

Annual revenue of Lex Autolease 2011-2024:

This points to a market where scale, funding access and fleet relationships are becoming more important.

Leasing providers should measure acquisition cost and lifetime value separately for business and personal leasing, because the economics are moving in different directions.

Search demand still matters, though the audience is changing

Search remains central to automotive research and brand discovery.

Google’s audience data shows that 54.7% of car buyers used search engines for online product research, and 38.7% used search engines for brand discovery between Q1 2024 and Q3 2025.

This means leasing providers still need strong organic and paid visibility.

The priority is to build separate journeys for business leasing and personal leasing, with different landing pages, finance messaging and conversion measures.

What leasing providers should do next

Business leasing is where resilience is strongest in 2026.

Personal leasing still has demand, though that demand is more price-sensitive and harder to convert.

Leasing brokers, OEMs and funders should shift more budget toward business leasing, measure each segment separately and use EV demand as a key route into fleet growth.

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information