- 2.4 million monthly EV searches, yet 70% of marketing spend goes to brand channels buyers don’t use.

- Search language reveals three distinct buyer mindsets: charging anxiety (“EV”), affordability (“electric car”), compliance (“electric vehicle”).

- 35% of EV searches are about charging, but this appears in less than 10% of OEM messaging.

- BYD wins search by answering buyer questions directly (price, comparisons).

- Legacy OEMs lead with brand storytelling that doesn’t appear in search at all.

Search Appetite at Scale: The Market Opportunity Being Missed

Over 2.4 million EV-related searches happen every month across the UK. Active buying intent, research behaviour, and decision-making happening in real time.

Yet walk into most automotive marketing departments and ask how much budget is allocated to answering these 2.4 million monthly searches, and you’ll find the answer is remarkably small.

Most of that search volume doesn’t happen on brand sites, in YouTube ads, or via premium publisher partnerships. It happens on Google, in comparison tools, on Reddit threads, and in YouTube reviews. It happens late at night when someone is deciding whether an EV actually makes sense for them, or when they’ve already decided they want an EV and are narrowing down which one.

Search data reveals the largest opportunity in automotive marketing right now isn’t brand awareness, it’s how answers align with search.

How Search Language Reveals What Buyers Actually Care About

This is where most automotive marketers get it wrong.

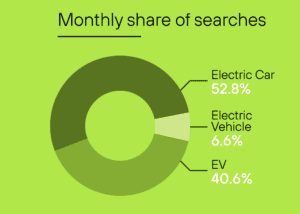

According to UpShift’s EV search research, the UK’s 2.4 million monthly EV searches break down into three distinct linguistic patterns:

- “EV” (1.3 million monthly searches): Infrastructure-led language. These searchers are asking about chargers, charging costs, home installation, tariffs, and nearby stations. The anxiety is practical: Can I actually use this thing?

- “Electric car” (1 million monthly searches): Consumer-facing, purchase-led language. These searchers are asking about deals, affordability, best options for families, and comparisons between models. The anxiety is financial: Can I afford this?

- “Electric vehicle” (162,000 monthly searches): Formal, policy-led language. These searches spike during government announcements. They’re asking about tax, mandates, grants, and fleet compliance. The anxiety is compliance: What does this mean for my business?

The same person might search for all three of these things over the course of their buying journey, but most automotive marketing treats them as a single, undifferentiated audience.

The result? A potential customer searches “EV charging cost near me” looking for a practical answer, and sees a brand ad about “the future of driving.” The customer is trying to solve a problem, but the brand is telling a story.

The Search Visibility Crisis: Where Legacy OEMs Are Invisible

Some of the world’s largest automotive companies are barely visible in EV search despite massive ICE market share and substantial marketing budgets.

The Legacy OEM EV Visibility Index (which measures monthly searches combining brand name + “electric”) reveals the gap:

What search shows:

- Renault: 81,000 monthly searches

- BMW: 64,000 monthly searches

- Volkswagen: 50,000 monthly searches

- Hyundai: 54,000 monthly searches

- Ford: 57,000 monthly searches

The invisible leaders:

- Nissan (inventor of the mainstream EV with the Leaf): 24,000 monthly searches

- Vauxhall: 29,000 monthly searches

- Mazda: 4,700 monthly searches

The table below shows:

- EV Search Volume (monthly average): The total demand for brand + electric queries in the UK.

- Keyword Count: The number of unique search queries captured for each brand.

These companies have brand recognition, dealer networks, and marketing budgets. Yet when buyers search for electric car information, these brands are largely absent from the search conversation.

The barrier isn’t distribution or product quality – It’s a messaging misalignment. These companies built their EV strategies around incremental product launches and legacy brand extensions. They didn’t build search-first content strategies designed to win the research moments when buyers are most motivated to act.

Why Search Visibility Matters More Than Brand Strength

A buyer searching “electric car comparison” doesn’t think about Ford’s legacy or Nissan’s history. They’re in research mode, ready to evaluate options and look for answers, not stories.

When Ford and Nissan aren’t visible at that moment, someone else’s brand becomes top of mind. And in a category where trust is still fragile, top-of-mind often becomes the shortlist.

This is where the search gap becomes commercial: legacy OEMs are spending marketing budgets on brand awareness and cultural positioning while losing the research moments when buyers are actually making decisions.

Tesla, by contrast, dominates not just through product but through search moment visibility. With 3.2 million monthly searches across models, charging, financing, and comparisons, the brand owns the research space because it shows up when buyers are looking.

BYD entered the market in 2023 and reached 882,000 monthly searches by 2025, but not through premium campaigns – through visibility at the moments when UK buyers were searching for price, comparisons, and reviews. Supply-led, search-aligned, effective.

The Real Cost: Why Invisibility Compounds Brand Strength Losses

For legacy OEMs, this invisibility creates a vicious cycle.

A buyer considering an EV doesn’t start with brand loyalty, they start with uncertainty. They research. And if your brand isn’t visible during that research, a competitor’s is. By the time they move to consideration, the shortlist is already set. Brand strength doesn’t matter if you weren’t in the research conversation.

This explains the paradox: Nissan invented the Leaf. It should own EV search, but instead, it’s invisible. Ford and Vauxhall have decades of automotive credibility, yet when someone searches “best affordable electric car,” these brands don’t show up.

Meanwhile, BYD entered the UK in 2023. It had zero brand recognition, but it showed up in search with price points, comparisons, and reviews. By 2025, it had 882,000 monthly searches and a higher visibility than Nissan, despite a fraction of the brand equity.

Search visibility becomes the baseline for consideration. Brand strength only matters if you’re already in the running.

The Strategic Reality: Search-First or Fade

Legacy OEMs face a choice they may not recognise they’re making:

Option 1: Search-first content strategy

- Build SEO-led content answering the exact questions buyers are searching

- Position EV advantages around what buyers actually care about (charging, cost, reliability, not innovation narrative)

- Redirect 15-20% of brand budgets toward search-aligned content

- Measure success by research-phase visibility, not just awareness metrics

Option 2: Remain invisible in research, hope brand carries the sale

- Continue betting on brand awareness and emotional connection

- Accept that you’ll lose the research phase to more visible competitors

- Win only the buyers who already know you, not the researchers exploring options

Legacy OEMs built their EV strategies around incremental product launches and heritage brand extensions. They didn’t build search-first content systems, and that’s the core miss.

What to Do: Two Moves to Reclaim Search Visibility

- Build Search-Owned Content That Answers Documented Buyer Questions

If your search data shows buyers are anxious about charging infrastructure, build content specifically addressing that. “EV charging options by region.” “Home charging installation costs.” “Public charging networks near [dealer locations].” Not inspirational storytelling. Direct answers.

If they’re concerned about the total cost of ownership, own that conversation. “EV running costs vs petrol cars.” “Battery degradation myths.” “Residual value comparison.” Match search intent with your answer.

- Reposition Your EV Narrative Around Search Reality, Not Brand Story

Your brand narrative might be “innovation” or “sustainability.” But when someone searches “best value electric car” or “most reliable EV,” they’re not looking for innovation. They’re looking for reassurance. Lead with what your search data shows buyers actually care about, not what your brand story prefers to tell.

This doesn’t mean abandoning brand strategy. It means ensuring that when a buyer is in research mode and searching for the information that will drive their decision, your brand shows up with an answer.

Tesla doesn’t win search because it invented EVs, but because it shows up in 3.2 million monthly searches across models, pricing, charging, and comparisons. It meets buyers in their research moments.

BYD doesn’t win search because of brand heritage; it wins because every model launch, every price announcement, every comparison question is answered. Supply-led, research-aligned, visible.

Legacy OEMs can do this. They have the products, distribution, and credibility. What they’re missing is the search strategy that makes that strength visible at the moment when buyers are actually researching.

The Search Gap Is a Visibility Gap

The 2.4 million monthly EV searches represent a massive research opportunity. Most of that volume happens outside branded spaces, with queries answered by aggregators, YouTube reviewers, and comparison sites.

Legacy OEMs built their business by controlling the sales conversation. They can’t control search, but they can show up in it.

Brands that align their content and messaging with search intent will own the research phase. Brands that don’t will remain invisible at the moment of maximum buyer motivation, which means maximum competitor opportunity.

The search gap isn’t about the car. It’s about whether you’re visible when the buyer is looking.

Want the full breakdown of trends?

👇

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information