UK EV search is already telling a different story to last year’s sales data.

Not about total demand but about shape, status and taste. SUVs still dominate volume, hatchbacks are fading from consideration and saloons and fastback-style sedans are quietly regaining momentum.

This matters because segment preference tends to lock in before registrations move. By the time sales data catches up, the opportunity has usually passed.

SUVs: The Default Choice While Uncertainty Persists

Electric SUVs dominate search because they feel reassuring. Not reassuring in a technical sense but reassuring in a psychological one.

Range anxiety, charging friction and resale concerns haven’t disappeared. Larger cars promise control, flexibility and security, whether or not they always deliver it in practice. That promise is enough to anchor demand.

Mid-size and large electric SUVs account for the highest share of model-level searches. The Tesla Model Y sits at the centre of that gravity, with the Skoda Enyaq, Kia EV9 and Hyundai Ioniq 5 close behind.

This isn’t hype-driven interest but it’s structural demand.

When buyers feel uncertain about new technology, they default to familiar formats. SUVs feel like a hedge because you get space, height, perceived safety and social validation in one package.

If you’re an OEM or broker without a credible electric SUV story, you’re asking buyers to take a leap they don’t want to take.

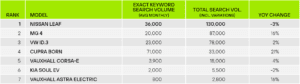

Hatchbacks: Still Searched, No Longer Desired

Hatchbacks haven’t disappeared, they’ve just stopped inspiring anyone.

The Nissan Leaf still attracts meaningful search volume, and so does the MG4. But both tell the same underlying story: flat growth, declining momentum, functional interest only.

People search these cars when they want the cheapest route into EV ownership, not because they want them. That distinction matters, interest without aspiration doesn’t compound, it plateaus.

Hatchbacks used to be the rational choice, though now they’re the compromise choice. In a market with expanding choice, compromise struggles to win.

If your EV proposition sits entirely in this segment, growth will be difficult, margins will stay thin, and brand pull will continue to weaken.

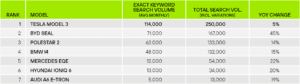

Saloons and Sedans: The Comeback Nobody Budgeted For

This is the shift few EV strategies budgeted for.

Electric saloons are growing faster than hatchbacks and, in some cases, faster than SUVs. The BYD Seal is the clearest signal, with search demand up more than 40% year-on-year. Polestar 2 continues to build momentum. BMW i4 and Hyundai Ioniq 6 show steady, durable interest.

These cars win for a simple reason, they make EVs feel desirable again.

Lower, sleeker and more efficient, they signal progress rather than compromise. They look like the future instead of a transitional solution.

They also sit neatly in the sweet spot for salary sacrifice and company car buyers. Strong ranges, cleaner benefit-in-kind maths and less visual bulk with more status per pound.

SUVs feel safe, saloons feel smart and right now, that distinction matters.

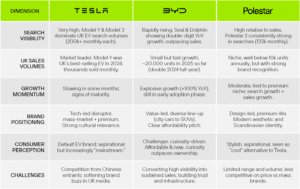

Why BYD Seal and Polestar 2 Are Outrunning Legacy Volume Cars

This isn’t about challenger brands versus incumbents, it’s about positioning versus inertia.

BYD Seal and Polestar 2 are growing because they answer a question older volume models no longer do, “what do I get if I move to electric now?”.

The Seal offers Tesla-adjacent performance at a sharper price, wrapped in a design that feels intentional rather than cost-led. Polestar 2 delivers restraint, clarity and credibility without shouting. Both feel considered but neither feels cheap.

That’s why search momentum is flowing toward them while older volume EVs plateau. Buyers aren’t just price shopping anymore, they’re identity shopping.

What This Means for EV Growth Teams

Segment choice is no longer a portfolio exercise but it’s a demand decision.

SUVs will continue to carry volume while uncertainty remains. Hatchbacks will continue to tick over, but they won’t lead growth. Planning as if they will is optimistic at best.

Saloons are where brand interest is compounding fastest right now. If you ignore them then someone else will capture that demand instead.

Search shows where permission exists before sales follow as at the moment, permission is shifting away from purely practical EVs toward cars that feel like an upgrade.

If your range, pricing or media strategy doesn’t reflect that, you’re fighting the market rather than riding it.

The UpShift Perspective

Most EV strategies are still built on assumptions formed when choice was limited and reassurance mattered more than aspiration.

Search behaviour shows those assumptions are expiring.

SUVs dominate because they reassure. Saloons are rising because they inspire. Hatchbacks are stuck in the middle.

If you want EV growth that lasts, build demand where aspiration is forming, not where habit is fading.

If you want to understand how this shift is playing out across your models, your competitors or your category, we should talk.

Want the full breakdown of trends?

👇

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information