In the UK, the electric vehicle market isn’t being defined by the old guard anymore. While legacy manufacturers are busy reshaping their product ranges, while EV-first brands are treating search data as a live demand signal rather than just a quarterly reporting metric.

The numbers are massive: over 2.4 million generic EV searches happen every month in the UK. This includes 1.3 million for “EV” and another million for “electric car.” But this isn’t just idle browsing. These searches represent people navigating real-time anxieties around range, price hikes, policy shifts, and model comparisons.

Right now, EV-first brands are punching way above their weight. They might not have the biggest sales footprint yet, but they are absolutely dominating the digital conversation.

Capturing Mindshare Before the Sale

To understand how this shift is playing out in consumer behaviour, we looked at branded search demand for leading EV-focused brands and traditional manufacturers.

Branded searches show which companies consumers actively seek out by name. In other words, they reveal which brands are winning attention, trust and curiosity as the electric transition unfolds.

The biggest gap between the newer EV brands and traditional manufacturers is how search visibility translates to sales.

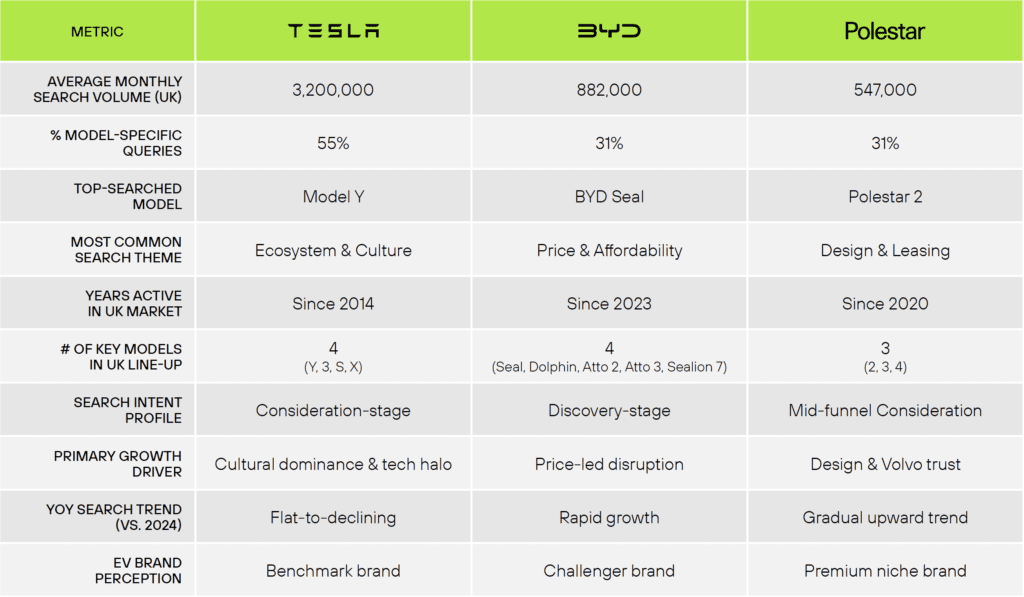

- Tesla is the heavyweight, pulling 3.2 million monthly searches. Crucially, 55% of that is model-specific. People aren’t just looking for “an electric car”; they are looking for a Tesla. This is high-intent, structured demand.

- BYD is the real disruptor. Despite only launching in the UK in 2023, they’re already generating 882,000 searches a month.

- Polestar follows with 547,000.

In both cases, their digital footprint is significantly larger than their current sales volume. This matters because search volume is a leading indicator. If you don’t own the digital consideration phase, your performance marketing has to work twice as hard to convert lukewarm interest.

Meanwhile, many traditional manufacturers face a brand identity challenge in the EV era. Their electric models are often introduced through separate sub-brands or scattered across multiple nameplates.

As a result, consumers may recognise the vehicle but not necessarily associate the parent brand with electric innovation.

Momentum: Who’s Gaining and Who’s Fading?

When you look at specific models, the shift in momentum is clear.

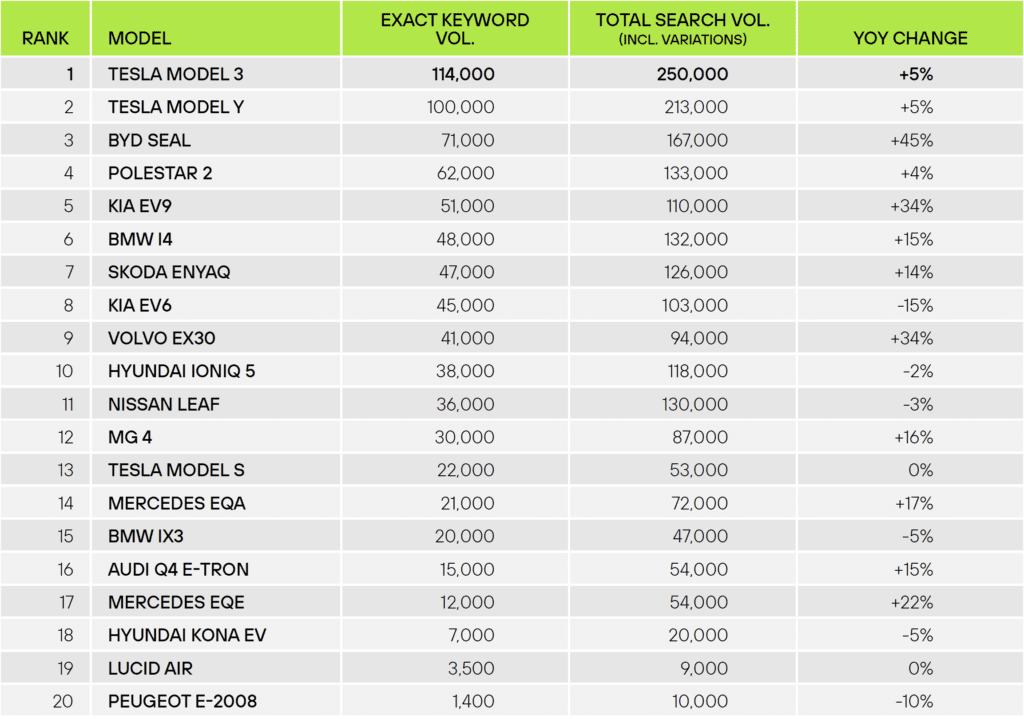

The Tesla Model 3 still leads with 250,000 monthly searches, but growth has flattened to +5%. The real movement is happening elsewhere:

- BYD Seal: +45% YoY

- Volvo EX30: +34% YoY

- Renault 5 E-Tech: Already +53% (and it hasn’t even launched yet)

On the flip side, the pioneers are losing steam. The Nissan Leaf is down 3%, and the Kia EV6 has dropped 15%.

These spikes aren’t just temporary trends, but they signal a broader shift in cultural relevance within the automotive industry.

For decades, traditional manufacturers dominated public attention and consumer curiosity. Today, much of that energy is moving toward EV-focused brands that feel more aligned with the future of mobility.

In search behaviour, that shift shows up clearly: consumers are increasingly looking for the brands that represent the electric transition rather than the companies trying to adapt to it.

The takeaway for incumbents? If your launch strategy doesn’t trigger a massive spike in search, you haven’t actually changed market perception, you’ve just run an expensive ad campaign.

Ecosystem Control vs. Category Chasing

There is a structural difference in how these brands manage the “funnel.”

Tesla owns the entire ecosystem. People search for “Tesla charging,” “Tesla Autopilot,” and “Tesla insurance.” Because they own the narrative, their cost per acquisition is naturally lower. They don’t have to bid as hard on expensive generic terms like “best electric SUV” because the customer is already looking for them by name.

BYD is currently winning the “curiosity” phase. About 31% of their searches are model-specific, while the rest are people asking: Is this brand legit? How does it stack up against a Tesla?

Legacy OEMs often fall into the trap of over-indexing on generic terms. They spend a fortune competing for “electric car” keywords because they haven’t built enough brand-specific demand. This is a margin-killer. You end up using your marketing budget to subsidize a lack of brand equity.

The Verdict: Clarity Wins

The advantage EV-native brands have isn’t necessarily a bigger budget, it’s a clearer story.

- Tesla is the default choice for tech dominance.

- BYD is the face of the “affordable” EV revolution.

- Polestar has carved out a niche in premium, Scandinavian design.

Legacy brands often treat electrification as a “feature” of their existing cars. But if consumers aren’t instinctively pairing your brand name with the word “electric” in Google, your EV strategy is still peripheral.

Waiting for registration data to tell you you’re losing share is a mistake. By the time the sales drop, the search data has already been screaming it for months.

Is your search data telling a story you don’t like? We help legacy brands pivot before the market does. Let’s talk.

Want the full breakdown of trends?

👇

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information