- Interest is mainstream, but confidence still lags

- Charging, cost and range remain the biggest anxieties

- BYD shows rising curiosity, but trust still needs building

- SUVs dominate because they feel like the safest EV choice

The UK now generates more than 2.4 million EV-related searches every month. Interest in electric vehicles has clearly moved into the mainstream. Consumers are researching models, comparing prices, checking charging costs, and exploring whether an EV fits their lifestyle.

The problem is attention is running ahead of confidence.

Search demand shows a market full of curiosity, uncertainty, and hesitation. People want electric cars but they are still working out whether they trust them enough to buy them.

This tension now defines the EV market.

Search Demand Is Massive, But Intent Is Fragmented

There are three distinct behaviours inside EV search demand:.

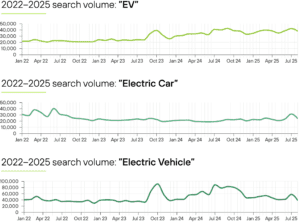

“EV” now generates 1.3 million monthly searches in the UK.

“Electric car” adds another 1 million.

“Electric vehicle” contributes 162,000 more.

Those numbers matter because the language consumers use reveals what they are actually thinking about.

“EV” searches cluster heavily around charging, tariffs, range, and infrastructure. Queries like “EV charger near me” and “EV charging cost” dominate the category. The audience is trying to understand ownership practicality.

“Electric car” searches behave differently. Users search for “best electric car”, “cheapest electric car”, and “electric car deals”. This is a more commercial mindset. Buyers are comparing products and narrowing options.

“Electric vehicle” searches skew toward tax, regulation, grants, and policy changes. This audience is often fleet-led or commercially driven.

The market is therefore much less mature than headline demand figures suggest.

High search volume does not mean high purchase readiness. It means millions of consumers are still trying to resolve uncertainty.

The Biggest EV Search Themes Are Still About Anxiety

One of the clearest findings from the data is that infrastructure and ownership concerns remain central to EV discovery.

The largest EV-related search clusters focus on charging cost, charger installation, charging locations, range, and tariffs. Consumers are still trying to understand whether ownership works in practice.

This matters commercially because most automotive marketing still assumes the market is already convinced.

A large percentage of EV budgets remains heavily weighted toward product messaging, launch campaigns, and model awareness. Search behaviour shows many consumers are still much earlier in the journey.

This creates a disconnect between what brands are promoting and what buyers are actually trying to solve.

OEMs, leasing brokers, marketplaces, and dealer groups should treat reassurance content as a demand capture channel rather than a support function.

Search demand around charging, battery life, home installation, public infrastructure, depreciation, and running costs is still huge because confidence gaps still exist.

The brands that reduce uncertainty fastest are likely to convert demand more efficiently over the next phase of EV adoption.

Search Interest Is Moving Faster Than Sales Momentum

Search visibility and sales performance are no longer moving at the same speed.

BYD is the clearest example.

The brand now attracts roughly 882,000 UK searches every month despite only entering the UK market in 2023. Queries around BYD Seal, Dolphin, and Sealion 7 have surged rapidly. The BYD Seal alone has posted 45% year-on-year search growth.

Yet UK sales volumes still lag far behind Tesla.

This gap tells us consumers are highly open to exploring new EV brands, but they are much slower to commit to ownership. Search behaviour around BYD is dominated by questions like:

- Is BYD reliable?

- Is BYD as good as Tesla?

- Why is BYD cheaper?

- Should I trust a Chinese EV brand?

The market is actively evaluating alternatives, but confidence still needs to be earned.

Tesla Shows What Mature EV Demand Looks Like

Tesla remains the clearest example of what confidence-driven EV demand actually looks like.

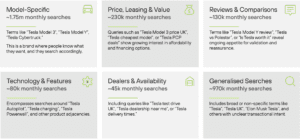

The brand generates more than 3.2 million UK searches per month. More importantly, 55% of Tesla search demand is model-specific.

Consumers are not searching “what is Tesla”.

They are searching “Tesla Model Y lease”, “Tesla Model 3 price”, and “Tesla Model Y review”.

That is much lower-funnel behaviour.

The contrast with BYD is important. Only 31% of BYD searches are model-specific. Most remain broad discovery queries.

Tesla’s position shows what happens once confidence barriers fall away. Search shifts from category understanding toward product comparison and ownership intent.

This transition matters commercially because it changes where marketing investment should sit.

Early-stage EV audiences need reassurance.

Mature EV audiences need conversion infrastructure.

Many brands are still treating both audiences the same way.

Cluster analysis of Tesla search queries shows how that visibility breaks down:

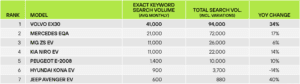

SUVs Continue To Win Because They Feel Safer

Search demand also reveals where confidence concentrates fastest.

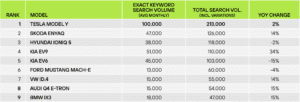

SUVs dominate EV search volume across the UK market. Models like the Tesla Model Y, Skoda Enyaq, Kia EV9, and Hyundai Ioniq 5 continue generating six-figure search volumes.

This dominance is not only about styling preference.

SUVs currently represent the safest emotional purchase in EV.

Consumers associate larger vehicles with practicality, range confidence, family usability, and better value retention. These perceptions matter heavily in a category where battery concerns and depreciation anxiety still exist.

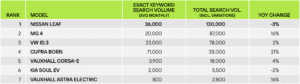

Meanwhile, traditional hatchbacks are losing momentum.

The Nissan Leaf still attracts significant search volume, but growth has flattened. The category increasingly feels functional rather than aspirational.

This creates a clear commercial implication for manufacturers and retailers.

The EV market is increasingly rewarding brands that combine reassurance with aspiration.

Consumers still want practicality. They also want confidence signals around technology, status, and future-proofing.

Mid-size / Large SUVs:

Compact SUVs / Crossovers:

Family Hatchbacks:

The Market Is Shifting From Awareness To Trust

The early EV market was

driven by novelty.

The next phase will be driven by credibility.

Search behaviour now shows a market actively validating claims rather than simply discovering products. Review searches, comparison searches, leasing searches, and ownership-cost queries are all growing.

This changes the role of automotive marketing.

Visibility alone is becoming less valuable.

Trust infrastructure is becoming more valuable.

That includes:

- Review visibility

- Lease transparency

- Charging education

- Ownership cost clarity

- Used EV reassurance

- Battery lifespan education

- Residual value confidence

The brands that simplify decision-making are likely to outperform the brands that simply generate awareness.

EV Demand Is Real. The Conversion Gap Is Real Too.

The data shows a UK market with enormous EV interest and unresolved consumer hesitation existing side by side.

This tension explains why search demand continues growing faster than confidence in some parts of the market.

Consumers clearly want electric vehicles.

They are still deciding which brands, technologies, price points, and ownership models they trust enough to commit to.

This distinction matters because it changes how growth should be approached.

Automotive businesses that continue treating EV marketing as a pure awareness challenge risk wasting budget at the wrong stage of the funnel.

The strongest opportunity now sits in helping consumers feel certain enough to act.

If this pattern is visible in search data, automotive brands should review whether current messaging answers the questions buyers are actually asking.

Want the full breakdown of trends?

👇

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information