Automotive marketing once rested on a bedrock of brand loyalty. Buyers traditionally followed a predictable path, choosing the badge their parents drove or sticking to a shortlist of familiar names they trusted. They would visit a local dealership, weigh two or three options, and sign on the dotted line.

That era is behind us.

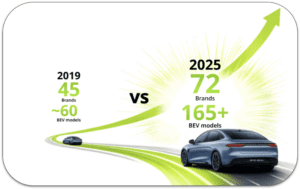

The UK automotive market is now busier, noisier, and far more complex than it has ever been. In 2019, there were 45 car brands available in the UK; today, that number has surged to 72. We have seen a proliferation of Battery Electric Vehicle models, with the total now past 165, with plenty more on the horizon.

For the modern buyer, choice is not a luxury; it’s a point of confusion.

With more brands, technical specifications, finance models, and ownership cost variables to juggle, the buying journey has become incredibly difficult to navigate. People are no longer just searching for a car; they are searching for validation, clarity, and answers to highly specific questions. If your digital strategy is not engineered to provide those answers, you are not just missing an opportunity; you are ceding your market share to the competitor who is.

The Shortlist Is No Longer Short

The traditional shortlist is breaking down.

Buyers are no longer comparing two or three familiar brands and choosing between them. They are actively weighing up established manufacturers against newer entrants, EV-first brands and challenger OEMs.

Google’s data show that the average number of brands a buyer compares has doubled from 4 to 8 in just four years. The average number of models being compared has also jumped from 11 to 16.

That matters because every extra comparison creates another opportunity for a buyer to change direction.

Someone may begin their journey with one brand in mind, but as soon as they start researching range, boot space, charging speed, finance options, reviews, delivery times or running costs, their consideration set expands.

Brand legacy is no longer a shield.

You cannot rely only on buyers who already know they want you. The real opportunity is now in the messy middle of the journey, where people are still deciding what matters most.

AI Is Becoming the Buyer’s Shortcut

Buyers are not using AI because it is shiny and new. They are using it because the decision has become harder.

When there are dozens of brands, hundreds of models and a wave of new EV considerations, people need help cutting through the noise. AI Overviews, AI Mode and search-led recommendation tools are starting to act like decision assistants.

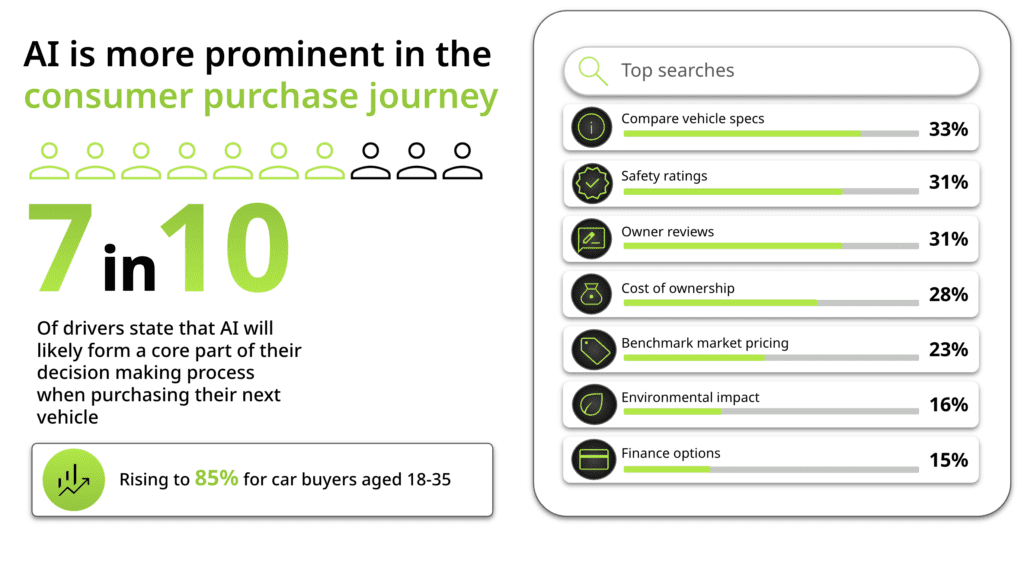

Google’s data show that 3 in 4 users say AI Mode and/or AI Overviews help them make faster, more confident decisions. It also shows that 7 in 10 drivers believe AI will form a core part of their next vehicle purchase journey, rising to 85% among 18- to 34-year-old car buyers.

That is a major shift.

People are not only asking “what car should I buy?” They are asking more specific questions around:

- Vehicle specs

- Safety ratings

- Owner reviews

- Cost of ownership

- Market pricing

- Environmental impact

- Finance options

This is where many automotive brands are exposed.

If your website content, vehicle data, finance information and comparison pages are thin, messy or difficult to understand, you make it harder for search and AI systems to recommend you.

That does not mean every brand needs to become an AI expert overnight. But it does mean the basics now matter more than ever.

Clear product information. Structured data. Useful comparison content. Transparent pricing. Strong reviews. Helpful finance explainers. Proper landing pages that answer real buyer questions.

These are no longer just SEO nice-to-haves. They are visibility assets.

Long Searches Are Now the Majority

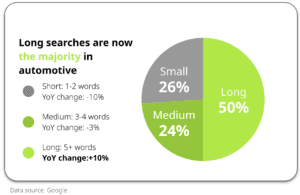

One of the most important findings in the data is the rise of longer, more specific searches.

Short 1–2 word automotive searches are down 10% year-on-year. Medium 3–4 word searches are also down. Long searches of 5+ words now make up 50% of automotive queries and are growing 10% year-on-year.

That tells us something important.

Buyers are not just searching for broad terms like:

“electric SUV”

They are searching for answers to specific problems, such as:

“safe electric SUV for families with large boot space and rapid charging under 50k”

“best electric car for motorway driving”

“EV salary sacrifice vs personal lease”

“cheap electric car with good range and low monthly payments”

“family SUV with low running costs and strong safety rating”

These searches may be smaller individually, but together they reveal exactly what buyers care about.

They show the fear. The need. The budget. The use case. The trade-off.

That is gold for a search strategy.

Challenger Brands Are Stealing Attention

This shift is also changing who gets noticed.

Google’s data shows that newer and challenger brands are gaining serious search momentum. Chery, Jaecoo, Omoda and BYD are all examples of brands attracting growing attention, while some established names are seeing flat or declining branded search movement.

That does not mean legacy brands are finished, far from it.

But it does show that attention is moving.

Buyers are more open to unfamiliar badges than they used to be. They are more willing to compare. They are more likely to be influenced by search results, reviews, pricing, finance information, YouTube content and AI-assisted recommendations.

This is not just an OEM issue either.

Dealer groups, leasing providers, salary sacrifice providers, finance brokers and car retailers all face the same challenge. If buyers are searching by budget, lifestyle, tax position, charging needs, ownership costs, and confidence signals, then visibility cannot be limited to the brand or model level.

You need to show up where the decision is being shaped.

The 70% Loyalty Blind Spot

The biggest warning sign in the data is this: 70% of consumers bought a different brand than the one they chose for their previous car purchase. That is huge.

It means loyalty can no longer be treated as a given. The buyer may have a history with your brand, but that does not mean you are safe.

With more choice, more comparison and more tools to help people evaluate the market, buyers are more willing to switch. They are not simply asking, “What does my usual brand offer?” They are asking, “What is the best option for me now?”

That is a very different question.

With more brand choice and AI simplifying complex research, comes more switching.

When loyalty drops, the marketing playbook has to change. The question is no longer just: “How do we protect our brand demand?”

It is: “How do we become useful, visible and convincing before the buyer has made up their mind?”

What Automotive Brands Should Do Now

The answer is not to rip up the entire strategy and start again. But automotive brands do need to rethink how they show up across search, content, video, feeds and measurement.

Here are the areas that matter most.

1. Build Around Buyer Questions, Not Just Model Names

Many automotive campaigns are still built around brand, model and generic category terms.

That still matters, but it is no longer enough.

Buyers are asking more detailed questions around range, charging, family use, boot space, safety, running costs, benefit-in-kind, salary sacrifice, finance, delivery times and monthly affordability.

Your search and content strategy needs to reflect that.

Instead of only targeting “electric SUV”, brands should be thinking about the actual problems behind the search:

- “Will this car fit my family?”

- “Can I charge it easily?”

- “Is it affordable to run?”

- “Is leasing better than buying?”

- “Will this work for my commute?”

- “What happens if I do mostly motorway miles?”

- “Is this better through salary sacrifice?”

That is where the buyer is making the decision.

The caution here is volume. Going broader can be dangerous if not properly controlled. If you open the door to every high-volume “best car” search without clear exclusions, strong landing pages and proper conversion tracking, spend can quickly become waste.

The opportunity is not just to chase more searches. It is to capture better intent.

2. Make Vehicle Data Easier for Platforms to Read

In the old world, your website was mainly built for people.

Now it also needs to be easy for platforms, feeds and AI-led systems to understand.

That means price, availability, finance examples, imagery, model specs and key features need to be clean, consistent and accessible.

For many automotive brands, this makes feed management one of the most important parts of search performance. Vehicle data is not just operational admin. It is a visibility asset.

If a competitor has cleaner pricing, better images, clearer financial information, and stronger inventory data, they make it easier for platforms to match them with the right buyer.

This is especially important for Google Vehicle Ads and Performance Max, where the quality of the feed can directly influence how well products are surfaced.

Messy data creates missed opportunities.

Clean data gives the platform more to work with.

3. Use YouTube as a Consideration Channel, Not Just Awareness

YouTube should not be treated solely as a brand-awareness line in a media plan.

In automotive, it is where people go to understand, compare and validate decisions.

The Google data shows that auto content is accelerating across YouTube, with 17 million in-market users for a car on YouTube in the last 30 days and 2.9 million hours watched on EV content in the UK, up 32% year-on-year.

That matters because people want to see the car, understand the features, compare options and hear practical explanations before they enquire.

Brands should be creating useful video content around:

- Range tests

- Charging explainers

- Model comparisons

- Finance explainers

- Ownership reviews

- Salary sacrifice guides

- “Best car for…” use cases

- Common EV concerns

- Interior and boot space walkthroughs

This content can support organic discovery, paid YouTube, Performance Max and remarketing.

But there is a catch.

Creative quality and creative volume matter. If your video assets are generic, static or too polished to be useful, performance will plateau. The brands that win will be those that can quickly test practical, helpful, and platform-native content.

4. Measure Lead Quality, Not Just Lead Volume

Not every lead is equal.

That sounds obvious, but many automotive accounts still optimise for form fills, calls, or enquiries without sufficient visibility into what happens afterwards.

A cheap lead that never converts is not efficient. It is just cheap.

Brands need to push more CRM and sales outcome data back into ad platforms, so campaigns can optimise towards enquiries that actually become valuable customers.

That means understanding:

- Which leads became appointments

- Which appointments showed up

- Which enquiries turned into sales

- Which finance products or vehicles created the most value

- Which campaigns drove poor-quality enquiries

- Which channels assisted the journey before the final conversion

This is where value-based bidding becomes important. The goal is not just more leads. The goal is more of the right leads.

However, this only works if the data is reliable.

If Consent Mode is not set up properly, if CRM data is messy, or if offline conversions are not being passed back accurately, automation will optimise towards the wrong signals.

Better bidding starts with better data.

5. Stop Giving All the Credit to the Last Click

The modern car-buying journey is not clean or linear.

A buyer may watch a YouTube review, read an EV guide, compare finance options, search for a competitor, visit an OEM site, return through a generic search, look at reviews, then finally enquire through a brand or retailer ad.

If you only measure the final click, you miss the journey that created the demand.

That can lead to bad budget decisions.

Upper and mid-funnel activity gets cut because it does not look efficient on paper. But in reality, it may be doing the work that helps the buyer build confidence.

This is why attribution and first-party data matter.

Data-driven attribution is not perfect, but it better reflects the journey than last-click attribution. When combined with CRM signals, it helps brands understand which touchpoints are actually contributing to valuable outcomes.

The brands that continue to judge everything by the final click will underinvest in the moments that shape the decision.

The Final Verdict: Are You Ready for the Shift?

The most significant change in automotive search is not just that buyers are searching more frequently; it is that they are searching differently. They are actively comparing a wider array of brands, using AI to simplify complex decisions, and asking specific, problem-led questions that many brands have historically ignored.

This creates a dangerous reality for organisations tethered to historical awareness or an over-reliance on last-click efficiency. Your legacy brand demand is no longer a shield against this volatility.

However, this also presents a major opportunity.

The brands that win in this next phase will not simply be the loudest; they will be the most useful, the most transparent, and the most frictionless. If your ecosystem is built to answer real buyer questions, surface clean vehicle data, and measure the full journey rather than just the final conversion, you will be the one they choose when the decision is made.

Do not wait for the market to force your hand. Audit your search, feed, and content architecture today. If your digital strategy cannot provide the answers a buyer needs to make their decision, you aren’t just invisible – you are actively helping them discover someone else.

Talk To Our Experts

Please submit your details and as much information as you can on what you would like to discuss:

required information